- April 23, 2026

- Becky Seefeldt

- 0

Can I Build my Own Payment Processor?

Every growing platform eventually hits the same inflection point: Should we build our own payment processor?

It’s a reasonable question. Payments sit at the center of customer experience, revenue, compliance, and product differentiation. And for companies operating in benefits, financial services, healthcare, or any environment where funds must be controlled, restricted, or made available under specific rules, the question becomes even more pressing.

But before deciding whether to build, buy, or embed, it’s important to understand what “payment processing” actually means, and why the answer isn’t as simple as it seems.

What is a Payment Processing Platform?

Most people think of payment processing as “moving money.” In reality, the movement of money is only a small piece of payment processing. But, it’s also two very different categories of movement and processing that occur.

1. Retail Payments (Receive Money)

This is the world of card acceptance, merchant acquiring, checkout flows and settlement into a merchant’s bank account. Stripe, Square, and Adyen live here. Their job is to help businesses receive funds.

2. Payment Processing Platforms (Make Funds Available for Use)

This is a different universe entirely. A payment engine controls:

how funds are stored

when they can be used

where they can be spent

how they move between accounts

how rules and restrictions are enforced

This is the world of benefits cards, multi-purse accounts, employer stipends, rewards programs, healthcare and insurance payments, government and programmatic spend. A payment processing platform doesn’t just move money — it governs it.

If your business needs to control funds, not just accept them, you’re in the second category.

And that’s where “building your own processor” becomes a much bigger lift.

What Does a Payment Processor Actually Do?

A true processor handles far more than authorization and settlement. At minimum, it must manage:

1. The Ledger (Incoming and Outgoing Flows)

The ledger is the orchestration engine that keeps every entity in sync by serving as the real‑time system of record for balances, debits and credits, holds, adjustments, purse‑level rules, and transaction history. It is where incoming and outgoing value flows converge, and where accuracy to the penny, auditability, and instant updates become non‑negotiable. In a multi‑party ecosystem, this is the layer that ensures every participant — employer, administrator, processor, and merchant — is operating from the same source of truth, which is ultimately what makes the entire experience predictable and trustworthy.

2. Compliance, Security, and Fraud Controls

A processor must meet strict requirements across PCI, KYC and KYB, AML, OFAC, network rules, data security, auditability, and dispute management. And, this is often where platforms underestimate the complexity. As organizations scale, any oversimplification in these areas tends to surface quickly as vulnerabilities (gaps in compliance, breakdowns in dispute workflows, or inconsistencies in how risk is managed).

The operational rigor behind these requirements is what keeps the ecosystem stable, predictable, and trustworthy. Platforms that treat them as table stakes rather than differentiators are the ones best positioned to grow without cracks forming under pressure.

3. Funds Availability Logic

Funds availability tends to spike complexity. Not only do processors need to consider how funds are accessed (cards, digital wallets, ACH, checks, and even third‑party payment apps), they must also determine when funds become available, how they can be used, which merchants are allowed, which categories are restricted, how rules vary by purse, program, or user, and how to handle reversals, returns, and adjustments across every channel.

This is where the system must enforce rules, and maintain consistency no matter how or where a transaction originates.

Building this correctly is not just difficult; it is what separates a stable, predictable system from one that cracks under real‑world volume.

4. Network Connectivity

To issue cards or move funds across any rail, a platform must secure card network certifications, establish BIN sponsorship, connect to settlement and clearing systems, support dispute and chargeback workflows, and enable tokenization and digital wallet functionality. These integrations are deep, technical, and tightly regulated, and they often take months or even years to build, certify, and maintain at scale.

5. Operational Infrastructure

A processor also has to support the operational backbone that keeps the entire system running reliably day after day, including customer service tooling, reconciliation, reporting, exception handling, program management, audit trails, and the uptime and redundancy required to ensure nothing breaks under real‑world volume. This is the invisible work that makes every transaction feel simple on the surface, even though the underlying machinery is anything but.

So… Can You Build Your Own Processor?

Technically, yes. Practically, it depends on your appetite for:

multi‑year engineering investment

ongoing compliance overhead

network certification cycles

operational staffing

24/7 monitoring

regulatory scrutiny

continuous audits

risk and fraud management

Most companies underestimate the scope by an order of magnitude.

Building a processor is not a feature. It’s a business.

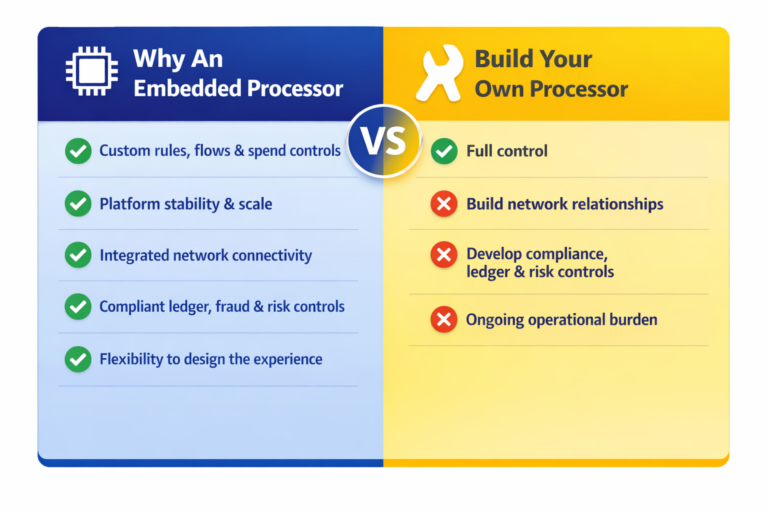

Why Embedded Payment Processing Is the Best of Both Worlds

This is where embedded processors change the equation.

They give you the control of building — custom rules, custom purses, custom flows, custom experiences, custom spend controls, and custom integrations — while delivering the stability of buying, including certified network connections, compliant ledgering, fraud and risk controls, settlement and reconciliation, operational tooling, ongoing audits, and regulatory alignment.

You get the flexibility to design the experience you want without carrying the full burden of becoming a regulated payments company.

It’s not build versus buy; it’s building on top of a platform purpose‑built for this.

If your business needs to control how funds move — not just accept payments — you’re operating in a category where traditional processors don’t fit and building from scratch is costly, slow, and risky.

Embedded payment processing gives you the infrastructure you need with the flexibility you want. It lets you focus on your product, not on becoming a processor.